Our search for equity diversifiers has us looking at free cash flow (FCF) as an important signal of business strength. FCF is the cash a company has remaining after operating expenses and capital expenditures. Free cash flow essentially represents the financial flexibility that enables all forms of value creation, from M&A to paying dividends.

The current FCF yield on the S&P 500 Index, at 2.65%, is the lowest in 25 years1, suggesting investors are paying a high price for the FCF they’re receiving.

The mega-cap companies that are spending big on the AI buildout are seeing their FCF draw down toward zero, with some now issuing debt to fund AI-related capex.2

This is not a flaw, in our view, but a strategy. Growth companies such as these may be expected to produce much higher cash flows in the future from the investments they are making today. In fact, aggregate S&P 500 FCF margins, which measure how well companies convert revenue into cash flow, are still near 15-year highs.3

Ultimately, the calculus is one of valuation and profitability, and it leads us to some other interesting and potentially overlooked portions of the equity market. Among them:

Energy: The current energy cycle could be elongated given two major developments:

- Massive demand for power from the AI data center buildout.

- A reshaping of the global supply chain amid recent geopolitical events in Venezuela and the Middle East.

In our view, the end of the Iran conflict is unlikely to quickly return energy supply to pre-war levels. Infrastructure damage, inventory depletion, slow reservoir ramp-up and shipping delays are likely to create a longer-term supply shock, resulting in structurally tighter supply and higher prices.

In a market in transition, global oil majors may use elevated FCF to pay down debt rather than increase drilling. Applying their financial flexibility in this way has a dual benefit: Paying down debt accrues directly to equity holders, and keeping supply in check as demand surges could support energy prices.

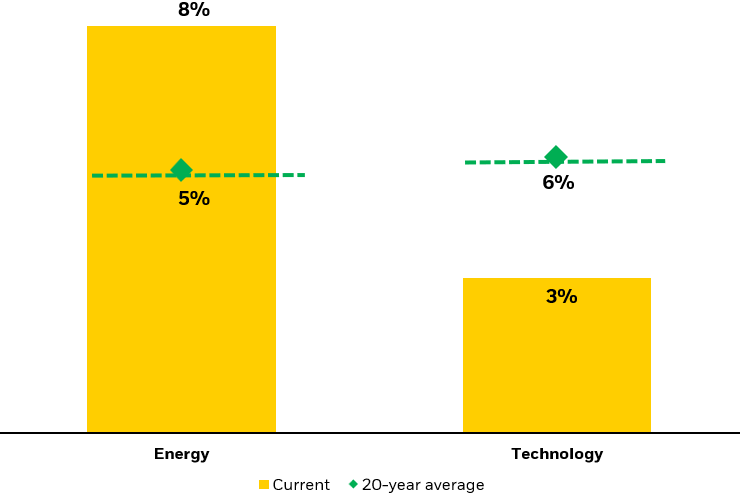

And yet, global energy stocks’ current FCF yield of 8% sits well above tech and the long-term average of both, as shown below.4 This attractive valuation, combined with potentially higher-for-longer oil prices, suggests to us that the investment case for the sector may be more durable than the market expects.