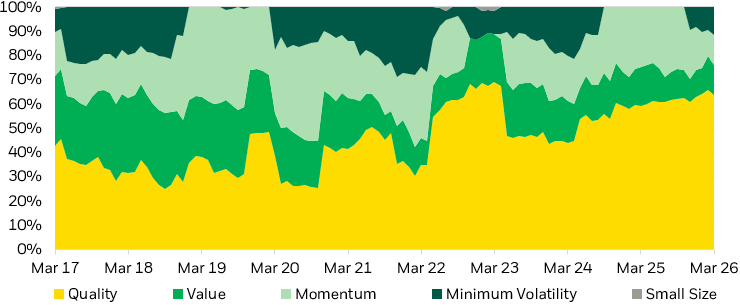

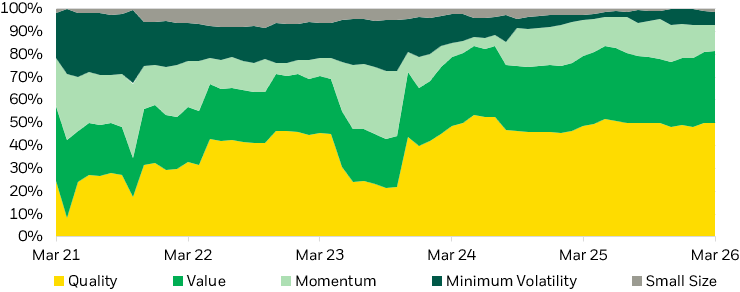

This shift in factor concentration may have important portfolio implications.

What were once more broadly diversified, market-capitalization benchmarks have evolved into portfolios dominated by a narrower set of companies and, by extension, a narrower set of performance drivers. For investors, this raises an important question: Are traditional equity benchmarks still delivering the diversification benefits they have historically provided?

We believe the answer is “no”.

When a single factor exposure dominates, diversification may weaken, and outcomes may become more dependent on the persistence of any given factor; for example, a period when Value stocks are doing well as a whole, such as after the bursting of the dot-com bubble.

As regime leadership rotates—and it inevitably does—portfolios with a high degree of concentration in any given factor may experience increased volatility and drawdowns when that single factor exhibits underperformance. For example, within U.S. equities, the Quality factor underperformed the broad market in 2025.2