These are key factors in determining risk tolerance, meaning how much market risk an investor is willing to accept in the pursuit of their financial goals.

Figuring out your risk tolerance isn’t easy, and it can change over time — just like other aspects of your life.

Imagine, for example, you’ve just arrived at a Fourth of July picnic, hosted by friends who are serious “foodies.” There are multiple kinds of main dishes to choose from — burgers, ribs, chicken, lentils, pulled pork, marinated tofu — as well as sides ranging from chickpeas to mac n’ cheese to potato salad to couscous. There’s also plenty of chips and dip, plus a whole separate table dedicated to desserts. There’s also a wide variety of beverages — with and without alcohol.

Deciding what to eat and drink, and how much, is a bit like choosing the asset allocation for your portfolio. And just like you eat differently when you’re younger, your asset allocation probably changes over time too.

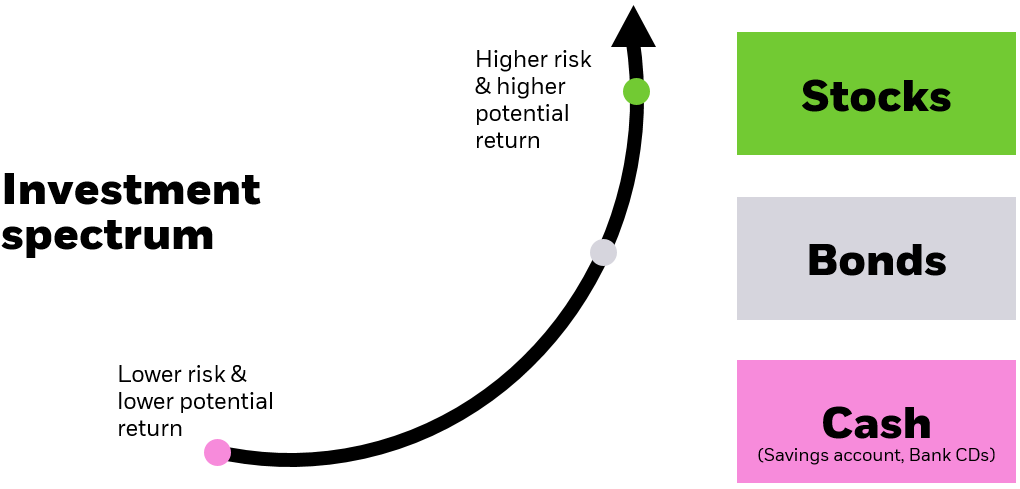

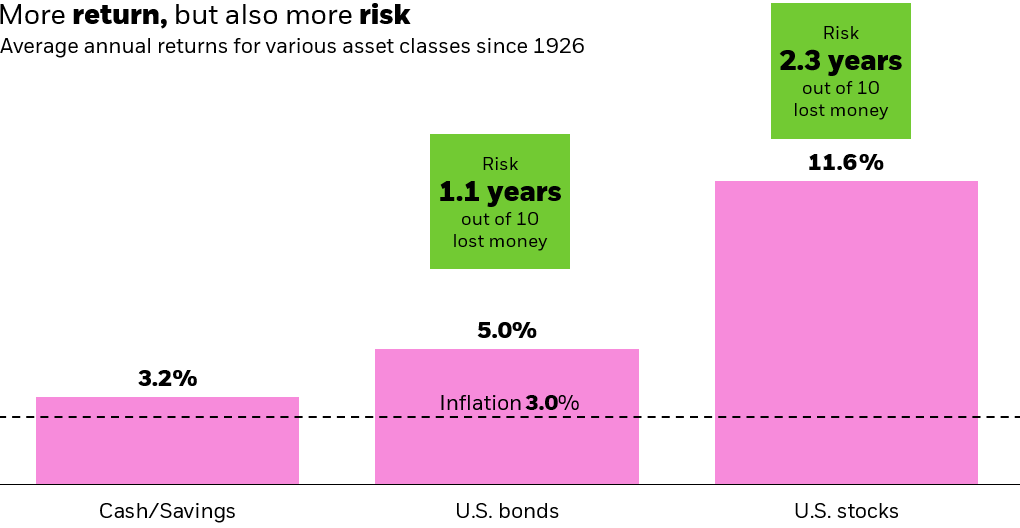

When I was in my 20s — and certainly as a teenager — I pretty much ate (and drank) whatever I wanted. That’s like being an “aggressive” investor. When you’re younger, you probably have more time in the market ahead of you and may be able to take more risk in the pursuit of higher potential rewards. (See figure 2 for historic performance of different asset classes.)