Key takeaways

- When investing for retirement, it’s critical to stay focused on after-tax returns. ETFs are generally tax efficient, which can help investors keep more of what they earn.

- Low turnover and insulation from the actions of other shareholders are keys to the tax efficiency of ETFs.

- ETFs held 30% of U.S. managed fund assets but accounted for less than 1% of capital gains distributions in 2025.1

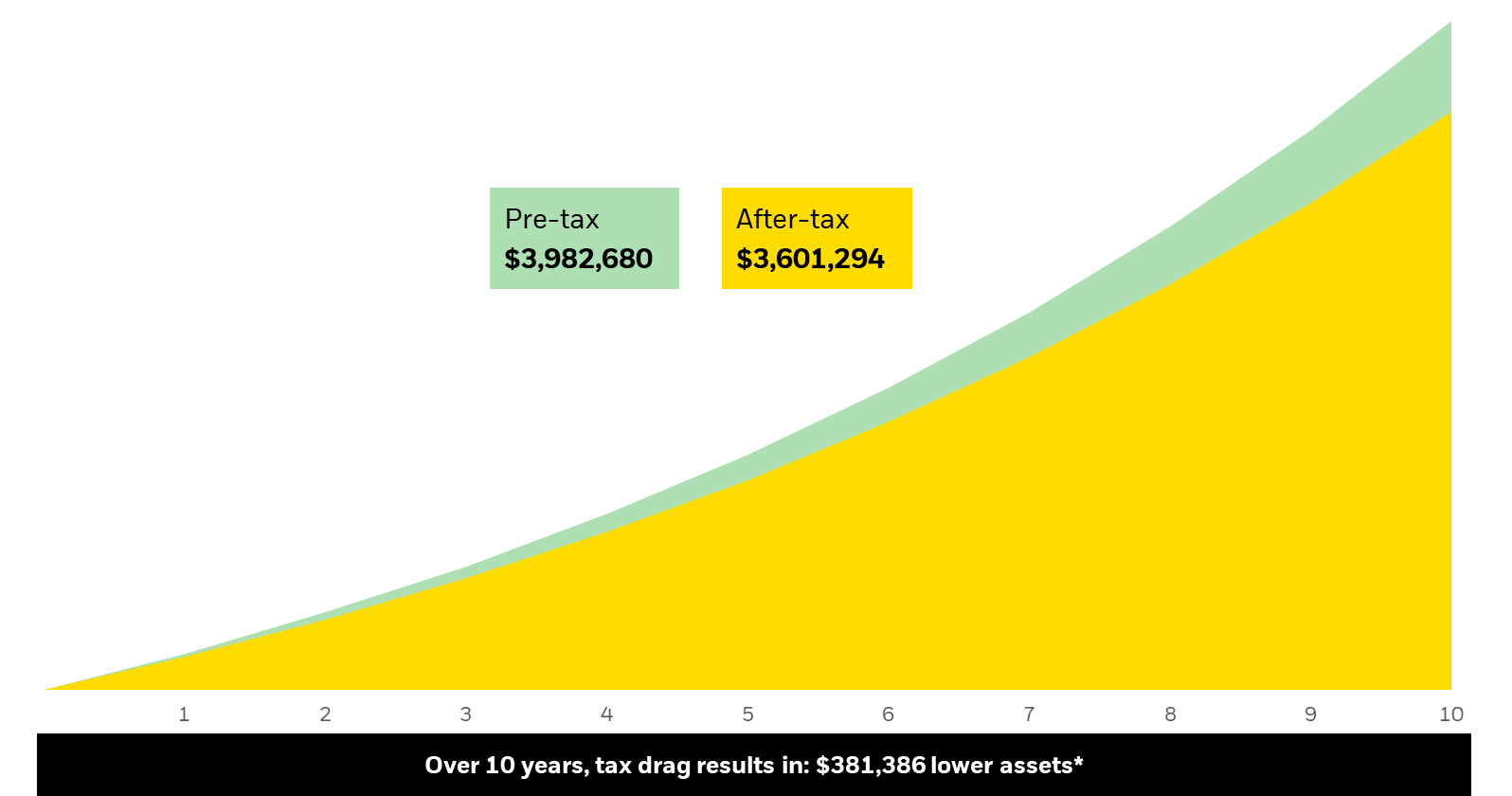

You’ve probably learned that keeping fees low can be a big driver of successful investing. And while keeping fees low is important, taxes may actually be more harmful to long-term returns than fund management fees.

For example, the average annual tax cost for investors using a financial advisor was 1.15% for calendar year 2025, more than triple the average portfolio fee of 0.37%. And while 1.15% may not seem like a big tax burden, a hypothetical $1,000,000 portfolio invested in the U.S. stock market would have suffered a tax drag of over $325,000 over the last decade.3