Updated: December 19, 2024.

Investing in lithium: Why now could be the right time

Jun 23, 2023 Industry

Key takeaways

- Lithium is among the most important metals required for electric vehicles and energy storage; as a transition to a low-carbon economy accelerates, demand is expected to increase exponentially, and companies involved may benefit.1

- The supply of lithium is constrained, given the complex extraction process and concentration of large deposits in South America, Asia, and Australia.

- Investors looking to gain exposure to lithium may want to consider ETFs that offer exposure to the entire value chain, including exploration, mining, processing, and compound manufacturing.

How to invest in lithium

As the transition to a low-carbon economy accelerates one metal stands out: Lithium. Lithium batteries are the default choice in electric vehicles (EVs), energy storage for solar and wind power, and consumer electronics, each of which present long-term growth opportunities. By 2026, It is predicted that 90% of lithium demand will stem from batteries, up from just 38% in 2016.2 However, expanding lithium supply is a complicated endeavor, leading to investment opportunities for companies that can meet the world’s growing demand.

3 reasons lithium demand is growing

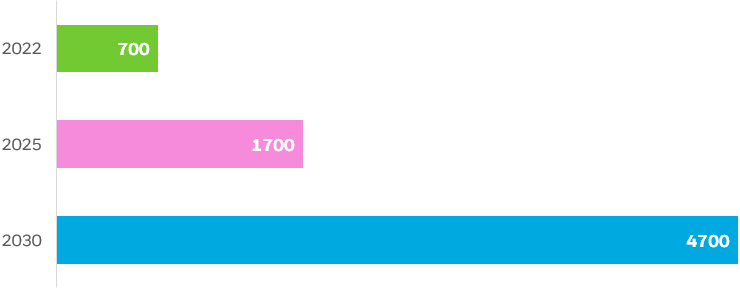

Lithium demand is expected to grow 7x between 2021 and 2030, driven by three key factors3: the growth of EVs, rising demand for renewable energy, and lithium’s use in consumer electronics.

Lithium-ion battery demand (GWh)

Source: McKinsey & Company. “Battery 2020: Resilience, sustainable, and circular.” 1/16/2023. Forward looking estimates may not come to pass.

Chart description: Bar chart showing lithium ion battery demand in 2022 and projected demand for 2025 and 2030.

EV Growth

Electric vehicles comprised approximately 18% of automobiles sold in 2023, up from 14% in 2022, and only 2% in 2018.4 As highlighted above, Automotive lithium-ion battery demand could increase by about over 30% annually from 2022 to, with the entire lithium-ion battery supply chain reaching a value of over $400 million, primarily due to growth in passenger EV sales.5 Lithium-ion batteries have become the default type of battery used in EVs because they have high energy density, long lifespans and require low maintenance. (Read more about the latest in EV innovation)

Growth of solar and wind power generation

The second key driver of lithium demand is the ongoing growth of solar and wind energy, with the amount of renewable energy capacity added to energy systems around the world growing by 50% in 2023, with solar and wind accounting for 95% of global renewable power capacity.6 Batteries are often paired with renewable energy generation to smooth out supply and demand fluctuations. They absorb excess solar or wind power when demand is low and discharge the stored energy when demand is high. Grid-scale battery storage capacity could expand as much as 35 – 44 fold between 2022 and 2030 under the IEA’s scenario where the world achieves net-zero carbon emissions by 2050.7

Compared to lead-acid batteries, which is an older technology, lithium-ion batteries offer several advantages. Lithium-ion batteries typically have up to 6x higher energy density, nearly 2x longer charge and perform better in cold weather environments,8 making them ideal energy storage solutions.

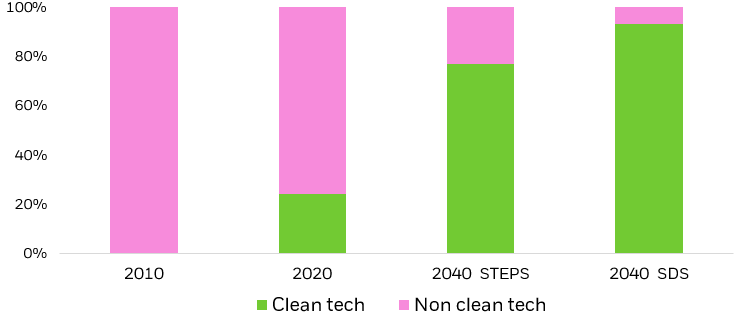

Share of clean energy technology in lithium total demand

Source: International Energy Agency, “The role of critical minerals in clean energy transitions” Forward looking estimates may not come to pass.

Chart description: Bar chart showing the share of lithium demand that stems from clean energy technologies. 2040 numbers are projections. The 2040 STEPS scenario is the stated policies scenario, an indication of where the energy system is heading based on a sector-by-sector analysis of today’s policies and policy announcements. The 2040 SDS scenario is the sustainable development scenario, indicating what would be required in a trajectory consistent with meeting the Paris Agreement goals.

Consumer electronics

The final component of growing lithium demand is its use in consumer electronics such as laptops and cellphones. While smart phones are ubiquitous in the U.S. with 82% penetration,9 they still have significant room to grow in countries like China and India, with 68% and 46% penetration respectively, and a combined 2.8 billion people10. As the digitization of the global economy continues, the lithium battery industry will have yet another tailwind from the continued growth of consumer electronics driven by the megatrend of growing wealth in emerging markets.

Lithium supply

We think it is important for investors to understand the complexities of the lithium supply chain as they consider potential investments. That is because demand for the metal is expected to significantly outpace supply in the coming years.11

Lithium is a soft, silver-white metal that is extremely light; it is typically extracted from lithium brine (accumulations of saline groundwater) or from spodumene ore (gemstone). Lithium supply is geographically concentrated, with 98% of lithium production in South America, Asia, and Australia.12 Given the concentration of the metal, geopolitical tensions have arisen which could constrain future access to lithium. For example, in the past two years, we have seen governments in Mexico and Chile initiate steps to nationalize lithium deposits.13 Additionally, government regulations around the globe that are designed to limit the environmental impact of mining limits companies’ ability to rapidly expand production, with the typical lithium project needing 3 – 7 years to finance and build.14

Despite these constraints, there are new technologies such as direct lithium extraction (DLE) which can bolster supply in the years to come. DLE is designed to skip the energy intensive mining process and directly extract lithium from brines, which can reduce both processing time and environmental impact. As a result of technologies like DLE, lithium supply is expected to grow 20% per year through 2030.15

How to invest in lithium

While we have extensively covered the supply and demand situation for lithium, it is important to note that raw lithium must go through several steps before it winds up inside a battery for an EV, solar storage, or other use case. Raw lithium from ores and brines gets processed and refined into lithium compounds, which become inputs for manufacturing batteries. The processing and refining are performed by lithium compound manufacturers, which are positioned to benefit as demand for lithium increases and more raw lithium needs refining.

Investors seeking to capture the lithium theme may want to consider ETFs that offer exposure to the full lithium value chain including:

- Companies involved in mining of lithium

- Companies involved in lithium compound manufacturing

Conclusion

We expect higher demand for lithium over the coming decade, as demand for EV batteries and renewable technologies continues to grow. Supportive government policies, growing consumer demand and constrained supply of the metal could help bolster companies involved with the lithium supply chain. Investors focused on electrifying their portfolios for the coming transition to a low-carbon economy may want to consider a diversified, ETF approach to lithium companies.