- To ensure a steady flow of income in retirement, transition your investment portfolio from growth-focused assets to income-generating ones.

- Create a detailed budget to track monthly expenses, and understand how to optimize withdrawals and minimize tax burdens.

- Consider using a tool, like our LifePath Spending Tool, to understand how much you might be able to spend in retirement each year.

KEY TAKEAWAYS

After years of diligently saving and investing, it’s finally time to take the off-ramp and cruise into retirement. Wondering how to smoothly switch gears from saving to spending? How to ensure your hard-earned savings last through the years?

Here are five steps to consider to help navigate this transition, and potentially make your retirement journey is as smooth and enjoyable as you envisioned.

1. SHIFT YOUR INVESTMENT PORTFOLIO

During your working years, especially in your younger years, experts recommend investing for growth when major swings in the stock market are less concerning, because your portfolio has time to recover. In retirement, when you rely on these investments for regular spending, experts recommend investing in more mature assets because wild swings in value can leave a long-lasting mark and potentially derail your retirement plans. The transition from growth to income should be a gradual process that focuses on increasing diversification to help reduce large swings in the value of your investments. This means shifting a portion of your investments from growth-oriented stocks to more mature assets, often in the form of dividend stocks, bonds and other investments with low correlation to high growth stocks. Think of it as tuning your engine from speed to fuel-efficiency.

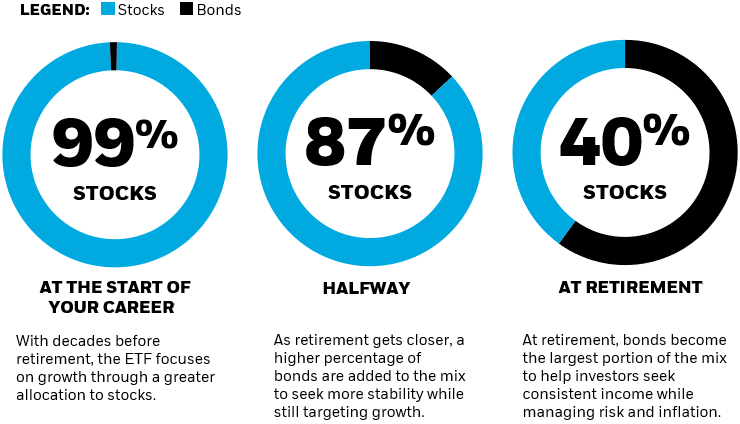

With the iShares LifePath Target Date retirement ETFs navigating this transition becomes easier. The ETFs are managed by a team of investment professionals and designed to automatically take more risk early on and gradually become more conservative as the target retirement date approaches. The result? Funds that seek the right risk at the right time, from retirement investing to retirement income. No need to make any changes, even in retirement. See below for how iShares Target Date ETFs evolve, adjusting the mix of your retirement portfolio adjustments for you, so you don’t have to.

Evolution of target date ETF investments

Asset allocations may periodically adjust based on an assessment of current market conditions. See the funds' prospectus for more information on each fund’s intended asset allocation mix over time. The principal value of the funds is not guaranteed at any time, including at the target date.

Chart description: "Start of Career" illustrates intended stock allocation with 40 years left until the target date. "Halfway" illustrates intended stock allocation with 20 years left until the target date. "Retirement" illustrates the stock allocation at the target date. Stock allocations may also include exposures to REITs.

2. SET A SPENDING LIMIT

When determining how much you can afford to spend in retirement, many retirees rely on “the 4% rule”1 — a common strategy which suggests withdrawing 4% of your portfolio in the first year of retirement, and continuing to do so in subsequent years while adjusting for inflation. This guideline aims to provide a steady income stream while reducing the risk of your tank hitting empty prematurely. It's like setting your cruise control to a steady speed.

Of course, if you’re interested in something more sophisticated than a rule of thumb, there are tools — like BlackRock’s LifePath Spending Tool — that can help you visualize how much you can spend each year by taking into account your age, savings balance, expected Social Security benefit, and more in just a few clicks.

3. MAP OUT A BUDGET

Expenses in retirement can be hard to visualize, while many assume retirement brings a simple reduction in expenses, the reality is far more nuanced. Some developments that can require careful consideration include:

- The need to replace employer sponsored healthcare coverage;

- Shifting housing costs as a result of downsizing or relocating, and;

- An abundance of leisure time may result in new hobbies or travel that need funding.

To create your new retirement budget, start by charting out expected expenses — from daily living costs to those bucket-list adventures. Be sure to add in buffers or additional funds for large but irregular expenses. Then, prioritize items on the list that must be covered and adjust the “nice to haves” in order to balance your annual budget. Creating a clear budget for expenses is like setting your GPS to ensure you don't wander off into overspending.

4. DON’T FORGET ABOUT TAXES

Navigating tax implications can add complexity but is an important part of making sure your investments last as long as you need them to. Withdrawals from certain retirement accounts, like traditional IRAs or 401(k)s, are taxable. These accounts also have required minimum distributions beginning at the age of 73. Managing your annual taxable income can help keep taxes down and more money going toward the things you want to spend it on.

5. MAKE REGULAR MAINTENANCE CHECKS

Just as you would regularly check your car, review your investment portfolio on an annual basis — looking at your investment objectives and your holdings to ensure alignment with your income needs and risk tolerance.

Here are a few common sources of risk to lookout for:

- Shift in spending habits: Veering away from your budget or covering a large, unexpected expense can deal a significant blow to your retirement security. Check your spending regularly to ensure you have accounted for all expenses and are sticking to your budget.

- Inflation: Inflation is like hitting an incline on your retirement journey — it eats up fuel by eroding the purchasing power of your savings. To counter its impact, include some investments with the potential to outpace inflation, like stocks or real estate, and keep your spending in check to ensure growth of your investments can keep up.

- Longevity risk: Thanks to advances in medical innovation, more people today are living into their 80s, 90s and beyond. With longer lifespans, the risk of outliving your retirement savings may present another important consideration.

Entering retirement should be full of joy and excitement. With thoughtful planning and regular adjustments, you can make this transition a fulfilling adventure. To begin switching from the fast lane to the exit lane explore target date ETFs which are designed to evolve over time, from retirement investing to retirement income. Prefer to build your own portfolio? Explore ETFs that can help you navigate risk. And remember to enjoy the view, make memories, and relish the freedom of your well-earned retirement!