Capital at risk. The value of investments and the income from them can fall as well as rise and are not guaranteed. Investors may not get back the amount originally invested.

Market Wrap

In Market Wrap, we look back at the events of the past month and outline what's on our radar for the month ahead.

Key Points

01.

Geopolitical risks resurface

Middle East tensions remain, putting pressure on oil and inflation expectations. NATO summit offered a more constructive signal of cooperation.

02.

Tech and energy stocks lead the way

US stock market profit growth is expected to be supported by semiconductors and energy.

03.

Events on our radar

Investors will be watching Middle East developments, upcoming central bank meetings and company profit reports for their potential impact on markets.

Geopolitical risks resurface

Early July saw the fragile Middle East ceasefire come under pressure after the US launched airstrikes and tightened sanctions in response to Iranian attacks on commercial shipping in the Strait of Hormuz, raising concerns that tensions could re-escalate. The flareup came just weeks after the US and Iran signed a memorandum of understanding (MoU) aimed at creating space for negotiations. While diplomatic efforts appear to be easing immediate tensions, the ceasefire remains fragile and periods of volatility are likely.

Oil prices had fallen following the MoU as investors became more optimistic that regional energy exports and shipping would gradually return to normal after significant disruption earlier this year. Recent events have reminded markets that this process may be uneven. A prolonged period of instability could delay the normalisation of energy markets and, if tensions were to escalate more seriously, renewed disruption to shipping and higher energy prices could contribute to inflationary pressures and increased market volatility.

The recent NATO summit has also been in focus, with President Trump reaffirming the US commitment to the alliance. Rather than announcing significant new spending commitments, the summit focused on implementation, with greater emphasis on defence procurement, industrial capacity and expanding production. Continued support for Ukraine and closer defence-industrial cooperation highlighted a broader shift from political commitments to long-term industrial delivery, reinforcing a more durable outlook for defence investment.

Tech and energy stocks lead the way

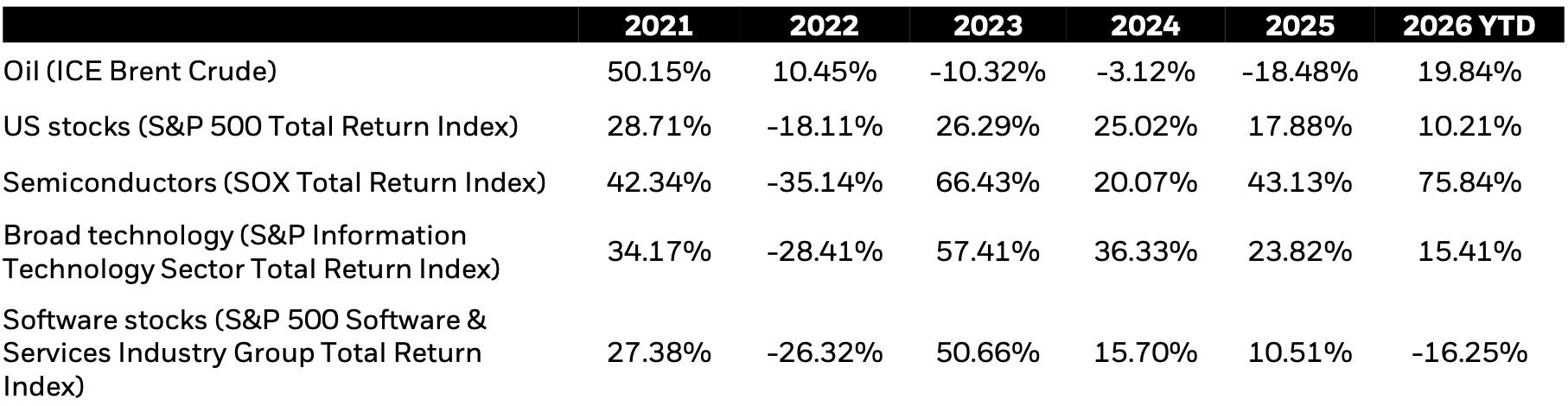

At the halfway point of the year, the S&P 500 is up 10%, with semiconductors, the chips and equipment powering AI systems, driving about half of the gains.1 Despite recent volatility and headlines, semiconductor stocks remain up around 75% this year.2 Software has been the biggest drag.3 Attention now turns to earnings season, when companies report their latest profits and forecasts for future earnings. Looking at earnings expectations, which refer to what analysts and investors think companies are likely to earn compared with the same period last year, S&P 500 companies are expected to grow profits by a combined 25% year-on-year. About half of that growth is expected to come from semiconductor and energy companies.4

Past performance is not a reliable indicator of current or future results and should not be the sole factor of consideration when selecting a product or strategy. Please see page 2 for historical performance data.

Events on our radar

Looking ahead, markets will focus on central bank meetings from the US Federal Reserve and the European Central Bank. Earnings season will test whether tech companies can meet high investor expectations, especially around AI spending. Developments in the Middle East, particularly around shipping and oil supply, will be key, as they could quickly translate into market volatility.

1,2,3 Source: BlackRock, Bloomberg, as of 30 June 2026. 4 Source: Bloomberg, as of 6 July 2026.

Performance of financial markets, 2021-2026 YTD

The figures shown relate to past performance. Past performance is not a reliable indicator of current or future results. Index performance returns do not reflect any management fees, transaction costs or expenses. Indices are unmanaged and one cannot invest directly in an index. Source: Bloomberg, as of 30 June 2026.

This document is marketing material: Before investing please read the Prospectus and the PRIIPs KID available on www.blackrock.com/it, which contain a summary of investors’ rights.

Investors should refer to the prospectus or offering documentation for the funds full list of risks.

Capital at risk. The value of investments and the income from them can fall as well as rise and are not guaranteed. Investors may not get back the amount originally invested.

Past performance is not a reliable indicator of current or future results and should not be the sole factor of consideration when selecting a product or strategy.

Changes in the rates of exchange between currencies may cause the value of investments to diminish or increase. Fluctuation may be particularly marked in the case of a higher volatility fund and the value of an investment may fall suddenly and substantially. Levels and basis of taxation may change from time to time and depend on personal individual circumstances.

BlackRock has not considered the suitability of this investment against your individual needs and risk tolerance. The data displayed provides summary information. Investment should be made on the basis of the relevant Prospectus which is available from the manager.

Regulatory Information

This document is marketing material and will expire 12 months after issue.

In the UK and Non-European Economic Area (EEA) countries (excluding Switzerland): this is Issued by BlackRock Investment Management (UK) Limited, authorised and regulated by the Financial Conduct Authority. Registered office: 12 Throgmorton Avenue, London, EC2N 2DL. Tel: + 44 (0)20 7743 3000. Registered in England and Wales No. 02020394. For your protection telephone calls are usually recorded. Please refer to the Financial Conduct Authority website for a list of authorised activities conducted by BlackRock.

In the European Economic Area (EEA): this is issued by BlackRock (Netherlands) B.V. is authorised and regulated by the Netherlands Authority for the Financial Markets. Registered office Amstelplein 1, 1096 HA, Amsterdam, Tel: 020 – 549 5200, Tel: 31-20-549-5200. Trade Register No. 17068311 For your protection telephone calls are usually recorded.

In Italy: For information on investor rights and how to raise complaints please go to https://www.blackrock.com/corporate/compliance/investor-right available in Italian.

For investors in Israel

BlackRock Investment Management (UK) Limited is not licenced under Israel's Regulation of Investment Advice, Investment Marketing and Portfolio Management Law, 5755-1995 (the “Advice Law”), nor does it carry insurance thereunder.

For Switzerland

This is Issued by either BlackRock Investment Management (UK) Limited ( or BlackRock (Netherlands) B.V.. BlackRock Investment Management (UK) Limited is authorised and regulated by the Financial Conduct Authority. Registered office: 12 Throgmorton Avenue, London, EC2N 2DL. Tel: + 44 (0)20 7743 3000. Registered in England and Wales No. 02020394. For your protection telephone calls are usually recorded. Please refer to the Financial Conduct Authority website for a list of authorised activities conducted by BlackRock. BlackRock (Netherlands) B.V. is authorised and regulated by the Netherlands Authority for the Financial Markets. Registered office Amstelplein 1, 1096 HA, Amsterdam, Tel: 020 – 549 5200, Tel: 31-20-549-5200. Trade Register No. 17068311 For your protection telephone calls are usually recorded.

For investors in South Africa

Please be advised that BlackRock Investment Management (UK) Limited is an authorised Financial Services provider with the South African Financial Services Conduct Authority, FSP No. 43288.

Any research in this document has been procured and may have been acted on by BlackRock for its own purpose. The results of such research are being made available only incidentally. The views expressed do not constitute investment or any other advice and are subject to change. They do not necessarily reflect the views of any company in the BlackRock Group or any part thereof and no assurances are made as to their accuracy.

This document is for information purposes only and does not constitute an offer or invitation to anyone to invest in any BlackRock funds and has not been prepared in connection with any such offer.

© 2026 BlackRock, Inc. All Rights reserved. BLACKROCK, BLACKROCK SOLUTIONS and iSHARES are trademarks of BlackRock, Inc. or its affiliates. All other trademarks are those of their respective owners.